Азиатский банк развития выпустил очередной Отчёт: «Экономические прогнозы для Азиатско-Тихоокеанского региона: апрель 2024 года». Согласно данному Отчёту экономика Узбекистана продемонстрировала заметный рост в 2023 году, поддерживаемый ускоренным расширением как в промышленности, так и в сельском хозяйстве. Однако эксперты прогнозируют замедление темпов роста в ближайшие годы в связи с различными факторами, включая увеличение администрированных цен и проведение структурных реформ.

Экономическая деятельность в 2023 году:

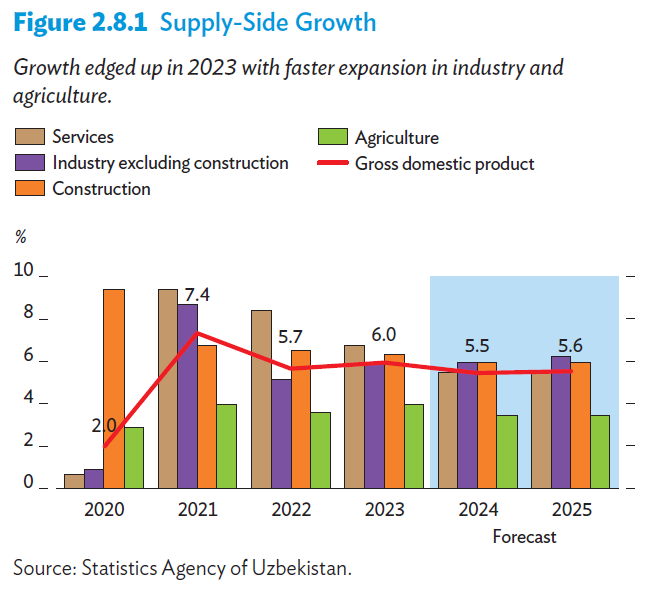

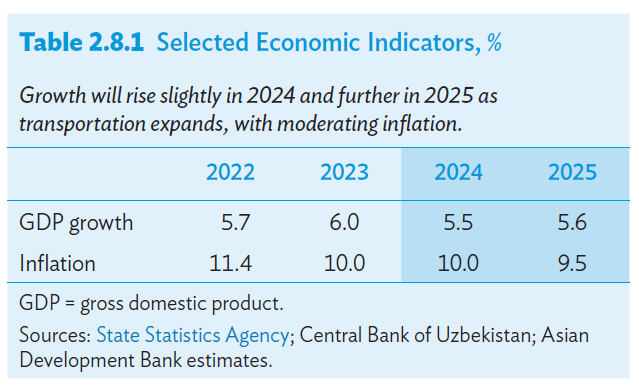

Ускорение роста: Государственное статистическое агентство сообщило о росте экономики с 5,7% в 2022 году до 6,0% в 2023 году. Этот рост в основном был обусловлен расширением деятельности как в промышленности, так и в сельском хозяйстве.

Динамика со стороны предложения: Промышленность показала сильный рост, особенно в области металлообработки, пищевой промышленности и текстильного производства. Однако добыча полезных ископаемых увеличилась незначительно из-за истощения запасов. Сельское хозяйство также пережило ускорение, благодаря спросу на хлопок, пшеницу, скот и сельскохозяйственные продукты.

Факторы со стороны спроса: Инвестиции существенно выросли, приводимые как частным, так и государственным сектором. Однако рост частного потребления замедлился из-за высокой инфляции и сокращения международных переводов.

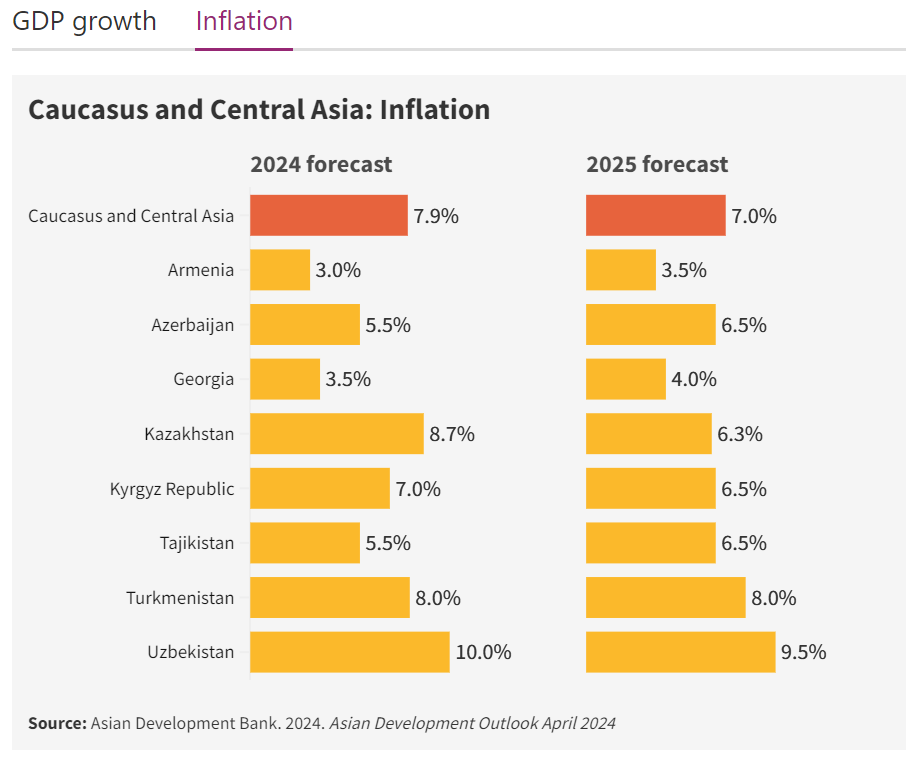

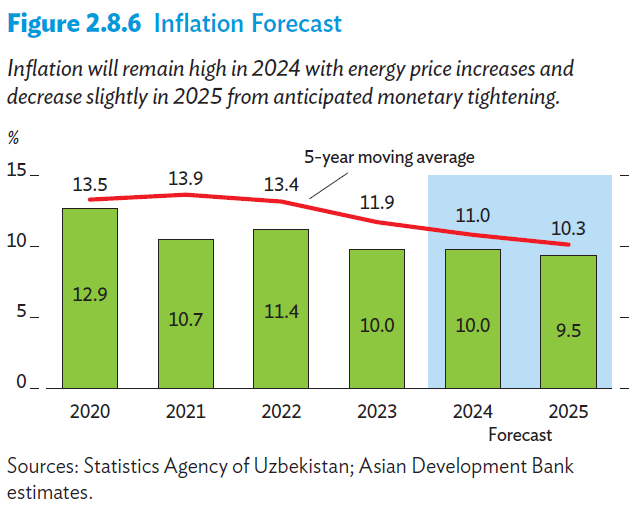

Инфляция: Тесная денежная политика и налоговые льготы на важные продукты питания способствовали снижению инфляции с 11,4% в 2022 году до 10,0% в 2023 году, хотя некоторые секторы столкнулись с давлением на цены, особенно в сфере услуг.

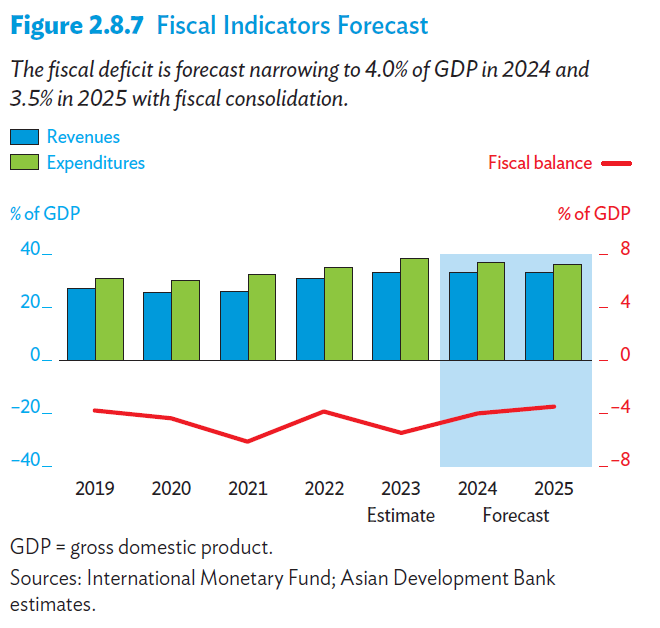

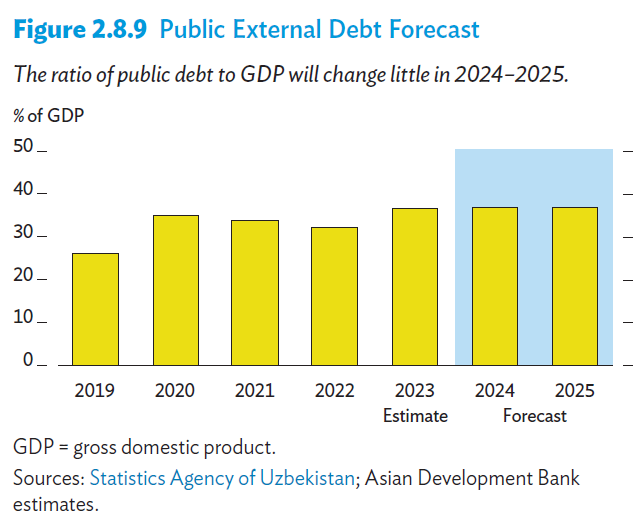

Фискальный дефицит: Фискальный дефицит расширился, что объясняется увеличением расходов, опережающих рост доходов. Внешнее заимствование финансировало значительную часть дефицита, что привело к росту государственного долга.

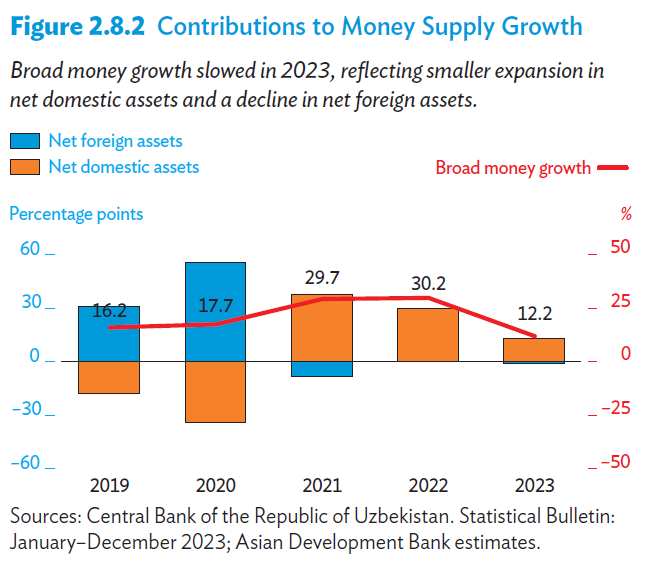

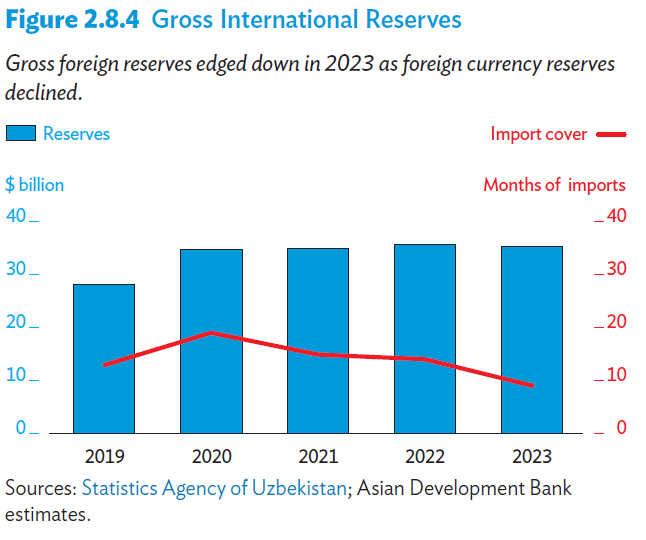

Кредитование банков и резервы: Кредиты в экономику расширились, при умеренном росте неплатежей по кредитам. Грубые валютные резервы немного снизились, но остались достаточными для покрытия импорта.

Экономические перспективы:

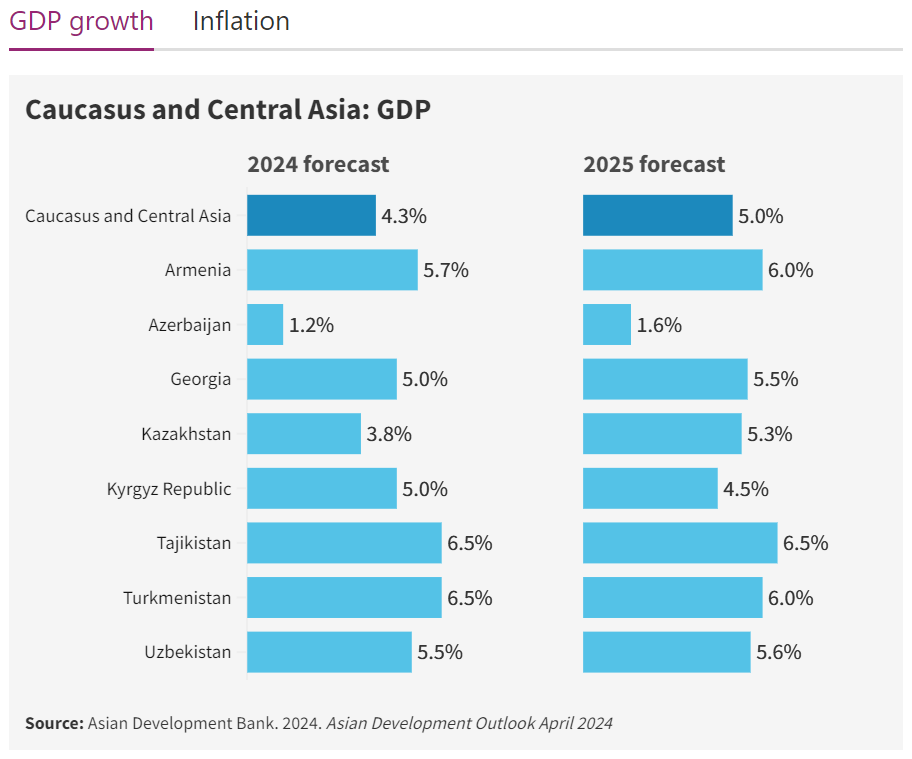

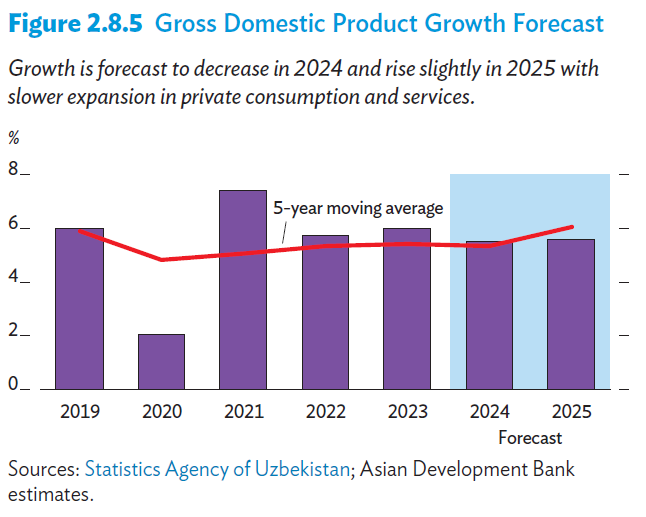

Прогнозируемый рост: Ожидается замедление темпов роста, особенно в сферах услуг и сельском хозяйстве, из-за увеличения администрированных цен и дефицита воды. Прогнозируется замедление до 5,5% в 2024 году перед небольшим повышением до 5,6% в 2025 году.

Проблемы со стороны спроса: Ожидается замедление роста частного потребления и инвестиций, вызванное структурными реформами и ограничением потребительского кредитования. Прогнозируется скромный рост государственного потребления, с увеличением инвестиций в ключевые сектора.

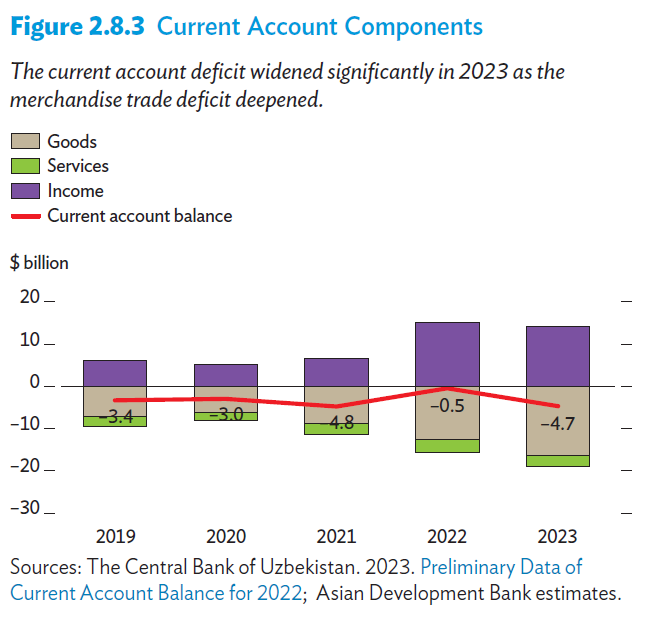

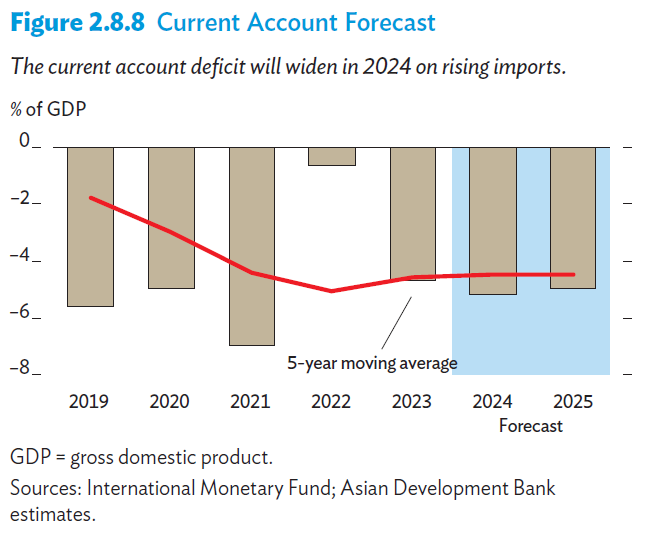

Торговый баланс: Ожидается увеличение импорта капитальных и промежуточных товаров, что приведет к расширению дефицита в чистом экспорте, компенсируя рост экспорта текстиля, продовольствия и туристических услуг.

Заключение:

Экономика Узбекистана проявила устойчивость и рост в 2023 году, поддерживаемые промышленностью и сельским хозяйством. Однако перед страной стоят вызовы, включая инфляционное давление, фискальные дефициты и дисбаланс внешней торговли. Решение этих проблем потребует продолжения усилий в области политики для поддержания стабильности и стимулирования устойчивого роста. Особое внимание уделяется политике зеленого развития, которая является критически важной для перехода страны к экологически чистой экономике, обеспечивая долгосрочное процветание и устойчивость.

С подробным отчётом можно ознакомиться по указанной ссылке:

Economic Forecasts: Asian Development Outlook April 2024 | Asian Development Bank